The CSRD is fundamentally changing how European companies report on carbon credits. No more netting, no more vague compensation narratives — instead, hard, auditable transparency on every carbon credit purchased. Companies that aren't prepared face a real greenwashing risk.

Short Answer: Under the CSRD, companies must report their carbon credits through ESRS E1-7, fully separated from their gross emissions. Carbon credits cannot be deducted from Scope 1, 2, or 3 emissions (E1-6) and cannot be presented as evidence of meeting reduction targets (E1-4). Companies must disclose per credit: volume in tCO₂eq, project type (reduction or removal), type of carbon sink, quality standard applied, share of EU-based projects, and whether the credit qualifies as an Article 6 corresponding adjustment. This strict separation is designed to prevent greenwashing and give stakeholders clear insight into both the company's actual emissions trajectory and the quality of purchased credits.

Who Is in Scope of the CSRD in 2026?

The scope of the CSRD was significantly narrowed in 2026 through the Omnibus I package, formally adopted on 24 February 2026. Thresholds have been raised to companies with more than 1,000 employees and net turnover exceeding €450 million. Listed SMEs (the original "wave 3") are now entirely out of scope.

In practical terms:

Wave 1 companies (large public interest entities already reporting under the NFRD) have been reporting since financial year 2024 and continue to do so. Member States may exempt companies below the new thresholds for financial years 2025 and 2026.

Wave 2 and 3 companies received a two-year deferral. Their first reporting now applies to financial years beginning on or after 1 January 2028.

Non-EU companies with net turnover above €450 million and a large subsidiary or branch in the EU also fall within scope, with reporting from financial year 2028.

EFRAG is currently finalising simplified ESRS, expected to reduce mandatory data points by approximately 60%. However, one thing remains unchanged: ESRS E1 (climate) continues to be the most scrutinised and technically demanding standard — even after simplification.

The Omnibus I package narrows the scope of the CSRD but leaves the core carbon credit disclosure requirements under ESRS E1-7 fully intact.

What Does ESRS E1-7 Require for Carbon Credit Reporting?

ESRS E1-7 is formally titled: "GHG removals and GHG mitigation projects financed through carbon credits." It has two pillars:

Pillar 1: Own GHG removals (insetting)

Report the total GHG removals and storage (in tCO₂eq) resulting from projects within your own operations or value chain. Think reforestation in your supply chain or technical carbon removal in your production process. Differentiate between biogenic (nature-based) and technological removals.

Pillar 2: Carbon credits from external projects

For carbon credits purchased on the voluntary carbon market (VCM), you must disclose:

Volume: total credits purchased and retired in tCO₂eq during the reporting period

Future retirements: expected volume under existing contractual agreements

Percentage breakdown by:

Reduction versus removal projects

Type of carbon sink (biogenic/nature-based or technology-based)

Quality standard applied per credit

Share of credits from EU-based projects

Share of credits qualifying as corresponding adjustments under Article 6 of the Paris Agreement

Quality substantiation: the credibility and integrity of credits used, referencing recognised quality standards

For companies making a GHG neutrality claim, additional requirements apply: you must demonstrate that the claim is accompanied by emission reduction targets (E1-4), that the use of credits does not undermine those targets, and that the credits are demonstrably credible and have integrity.

For companies with a net-zero target, you must additionally explain how residual emissions (after 90–95% reduction) will be neutralised — for example, through GHG removals in your own value chain.

Under ESRS E1-7, companies making a climate neutrality claim must prove that their carbon credits support that claim without undermining their reduction targets.

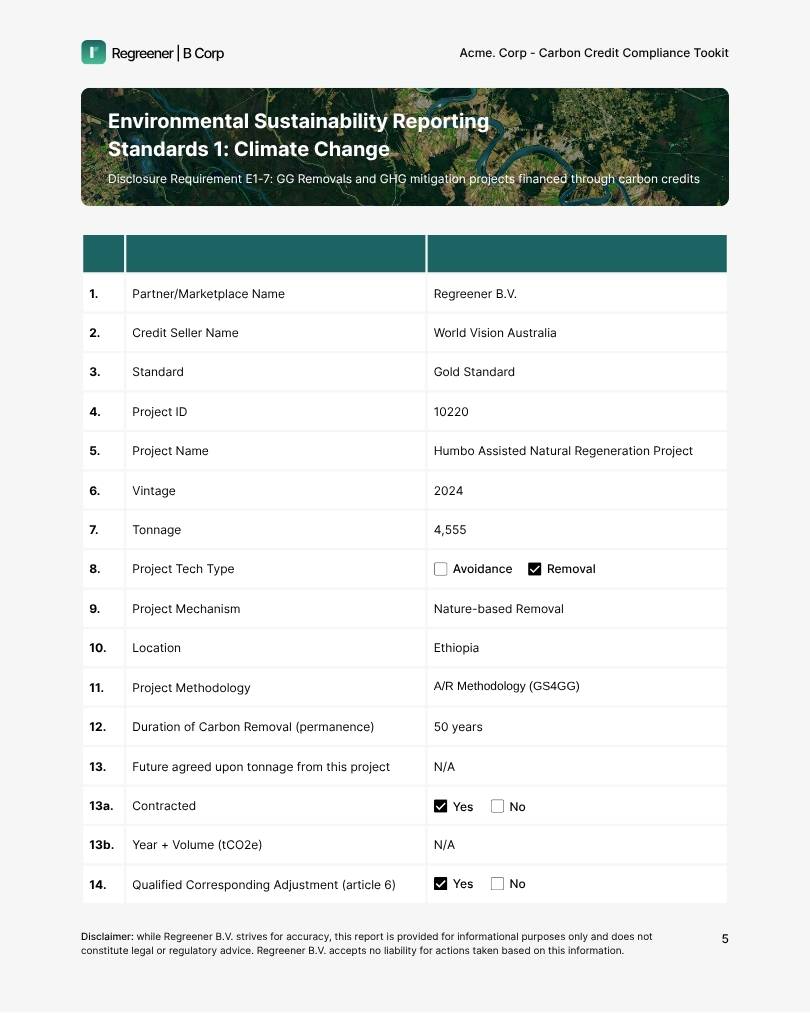

Regreener's Climate Strategy and Solutions team can provide you with a clear report containing the information you need to disclose on your use of carbon credits. That way you are well prepared when compiling data for CSRD. Here’s an example for a ARR credit purchase:

An excerpt from Regreener's template for CSRD reporting

What You Must Not Do: Anti-Greenwashing Rules for Carbon Credits Under the CSRD

The CSRD sets hard boundaries that every company with carbon credits in its portfolio must understand:

Carbon credits must not be netted against gross Scope 1, 2, or 3 emissions under E1-6

Credits must not be presented as a means to achieve emission reduction targets (E1-4)

You must not aggregate emissions and credits into a single combined figure

This is the core anti-greenwashing logic: stakeholders must be able to assess your actual emissions trajectory independently from what you offset. At Regreener, we advise our 200+ European clients to always position carbon credits as a complement to — never a substitute for — an ambitious reduction pathway. That's not just what the CSRD requires; it's what investors and regulators expect.

Quality Requirements: Where the CSRD Raises the Bar

The CSRD doesn't just ask whether you buy carbon credits — it demands transparency about their quality. This is where many companies are exposed. Research indicates that a majority of large European companies hold portfolios with relatively low-quality credits, often due to insufficient due diligence during procurement.

The term "recognised quality standards" is not precisely defined in the ESRS, but in practice it refers to:

Verification standards: Verra/VCS, Gold Standard, Puro.earth

Meta-standards: ICVCM Core Carbon Principles (CCPs) — the most authoritative quality benchmark for carbon credits globally

Quality criteria: additionality, permanence, avoidance of double counting, independent verification by accredited auditors

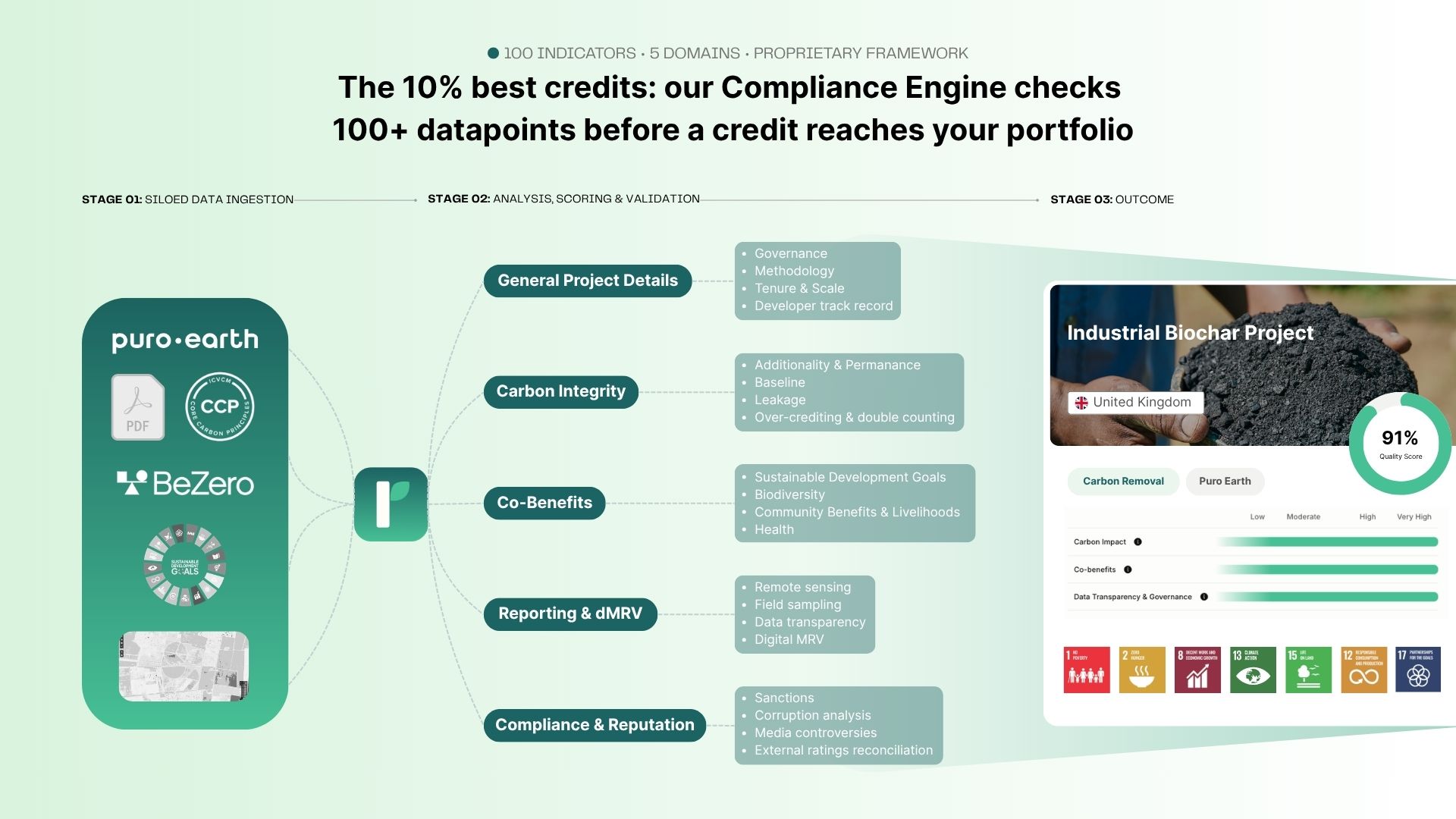

At Regreener, we evaluate every carbon credit project through our proprietary quality framework spanning over 100 data points across five domains: General Project Details, Carbon Impact, Co-Benefits, Reporting & dMRV, and Compliance & Reputation. This level of analysis is exactly what the CSRD expects — and what auditors will test.

Explore our Guide: the best Carbon Credit Projects of 2026

Learn about the latest best practices, high-quality projects and strategic options

How the CSRD Relates to Other Regulations

The CSRD doesn't exist in isolation. Three other regulatory developments directly affect how you report on carbon credits and which claims you can make:

EU Green Claims Directive (ECGT)

From September 2026, companies in the EU can no longer make unsubstantiated climate neutrality claims based on offsetting. Your CSRD reporting effectively becomes the factual underpinning of your climate claims. Companies subject to both directives must make their carbon credit reporting not just CSRD-compliant, but also resilient to scrutiny under the Green Claims Directive.

SBTi and Carbon Credits

The Science Based Targets initiative recognises carbon credits exclusively as a complement to direct emission reductions. Under the SBTi V2.0 draft framework, credits may only be used for residual hard-to-abate emissions after achieving at least 90–95% reduction. The SBTi calls this "Beyond Value Chain Mitigation" (BVCM) and actively encourages companies to contribute to climate action outside their own value chain through high-quality carbon credits.

ISSB/IFRS S2 Interoperability

The ESRS and IFRS S2 are largely interoperable. Companies already reporting under ISSB or CDP can take a "top-up" approach, adding only ESRS-specific data points. EFRAG and IFRS published detailed interoperability guidance in 2024 that supports this approach.

The combination of the CSRD, EU Green Claims Directive, and SBTi V2.0 compels companies to use carbon credits exclusively as a supplement to their reduction pathway, never as a replacement.

Practical Steps to Become Audit-Ready

1. Separate your data now

Ensure your GHG inventory and carbon credit records sit in separate systems or datasets. No combined spreadsheets. The auditor needs to see that gross emissions have been determined independently.

2. Document your procurement policy

Record the quality criteria you apply when purchasing carbon credits. Define minimum thresholds for additionality, permanence, and co-benefits. This becomes part of your E1-7 disclosure and demonstrates governance over your climate strategy.

3. Build an audit-ready evidence pack per project

Assemble per project: registry information from the Verra Registry or Gold Standard Impact Registry, verification reports, project design document (PDD), quality assessment, and retirement confirmation. Auditors under limited assurance (ISSA 5000) will request these documents.

4. Work with a specialist partner

Carbon credit reporting under the CSRD requires deep expertise in both the regulatory framework and the voluntary carbon market. A specialist partner helps you avoid greenwashing risks and makes your reporting audit-proof.

Want to know how your carbon credit portfolio scores against CSRD requirements? Talk to one of our experts and discover how Regreener helps you report transparently, audit-ready, and free from greenwashing risk.

Want to know which credits fit your company's climate strategy?

Book a free consultation today