Signing a carbon offtake means committing money and reputation to credits that, in many cases, do not exist yet. Over a 5 to 15 year term, the project can change, the registry can revise its methodology, and the developer can miss issuance targets. A carbon offtake due diligence checklist is how a serious buyer separates a project that will deliver from one that merely looks good on a pitch deck. This is the checklist we use at Regreener before we put a client's name on a multi-year contract.

The short answer

Carbon offtake due diligence covers six domains:

Project integrity

Verification and MRV

Delivery and volume risk

Contract terms

Counterparty and payment security

Ongoing monitoring.

Generic carbon credit checklists stop at project quality. Offtake diligence cannot, because the buyer carries delivery and project risk for the entire contract term. The contract clauses matter as much as the credit rating. Work through all six before you sign, and reassess at every issuance milestone after that.

One principle runs through the whole process. Validation confirms a project's design meets the methodology. It does not confirm the credits will be delivered. Everything below exists to close that gap.

1. Project integrity

This is where every checklist starts, and where most stop. For an offtake it is the foundation, not the finish line.

☐ Additionality is evidenced, the reductions would not have happened without carbon finance, with a documented baseline and barrier analysis.

☐ Permanence is addressed, with a stated durability horizon and, for nature-based projects, a buffer pool contribution against reversal.

☐ Leakage is quantified and deducted, so emissions are not simply displaced elsewhere.

☐ Methodology and registry are named and current (Verra VCS, Gold Standard, Puro.earth, Isometric, ACR, or CAR), with the specific methodology version recorded.

☐ Independent rating exists or is obtainable (BeZero, Sylvera, or Calyx Global). Treat an unrated project as a higher diligence burden, not a dealbreaker.

☐ The project aligns with the ICVCM Core Carbon Principles, or you understand exactly why it does not.

2. Verification and MRV

Measurement, reporting and verification is what turns a project's claim into a credit you can defend to an auditor.

☐ The monitoring plan is documented and the monitoring parameters are clear.

☐ A qualified, accredited VVB (validation and verification body) is engaged, and you know its track record.

☐ You can distinguish where the project sits between validation (design approved) and verification (reductions confirmed and issued). Pre-verification credits carry materially more risk.

☐ The vintage and issuance cadence are defined, so you know which years' credits you are buying and when.

3. Delivery and volume risk

In an offtake the buyer carries delivery risk for the full term, so this domain is where offtake diligence diverges hardest from a simple spot purchase.

☐ The developer has an issuance track record, or, for a first-of-kind project, a credible reason you should accept the additional risk.

☐ The delivery schedule is realistic against the project's actual timeline (planting, growth, capture, verification cycles), not against a best-case projection.

☐ A buffer or backup pool is available to cover shortfalls.

☐ The project's pre-issuance status is understood, including how long registry validation and verification might realistically take and what could delay it.

☐ You have modelled what happens to your own targets if the project under-delivers by 20, 40 or 60 percent.

4. Contract terms

The clauses are the part a generic checklist ignores and the part that decides whether your diligence actually protects you. A poorly drafted offtake can leave a high-quality project unable to help you. Read more about offtake contract terms here.

☐ The pricing mechanism is explicit (fixed, indexed, or escalator) with defined behaviour if the market moves sharply.

☐ Underdelivery and replacement clauses specify the remedy: replacement from a backup pool, financial compensation, or contract adjustment.

☐ Termination and default provisions set out the conditions under which either party can exit, and the consequences.

☐ Title transfer and retirement are unambiguous, you know exactly when ownership passes and who retires the credits in the registry.

☐ Corresponding adjustment treatment is addressed where relevant to your claims, since this can affect the credit's usability.

☐ Exclusivity, audit rights, and quality re-confirmation at delivery are included, so you can reject credits that no longer meet the criteria you signed for.

5. Counterparty and payment security

A long contract is protected less by how established the parties are and more by how tightly your money is tied to actual delivery. Strong structural safeguards de-risk an offtake even when a project or developer is early-stage.

☐ Payment is linked to delivery, milestone or on-delivery payments rather than a large upfront lump sum, so your capital is exposed only as credits are verified and issued.

☐ Where upfront funding is required, common for early-stage projects, it is protected by escrow, staged disbursement against verified milestones, or a performance guarantee.

☐ Credits are issued through the registry into your own account on delivery, so retirement does not depend on the counterparty's standing at that future date.

☐ The project developer's financial viability is assessed against the project's funding needs over the contract term, not just its current balance sheet.

☐ Governance, ownership and community consent are documented, particularly for nature-based projects on occupied or indigenous land.

☐ The advisor or broker structuring the deal is independent of the project developer, with no conflict of interest that could compromise the diligence on your behalf.

6. Ongoing monitoring

Diligence does not end at signature. An offtake is a relationship you manage for years.

☐ Milestone tracking is in place against the delivery schedule, with named checkpoints.

☐ Early-warning indicators are defined, so you spot under-issuance or quality drift before it derails the contract.

☐ An annual review of the project's status, rating and registry standing is scheduled.

"The mistake we see most is buyers running spot-market diligence on an offtake. They rate the project, sign the contract, and never look at the replacement clause. When the project under-issued in year three, the rating was right and the contract still left them exposed. On a multi-year deal, the clauses are the diligence."

Boris Bekkering - Commercial Director Regreener

How Regreener runs offtake diligence

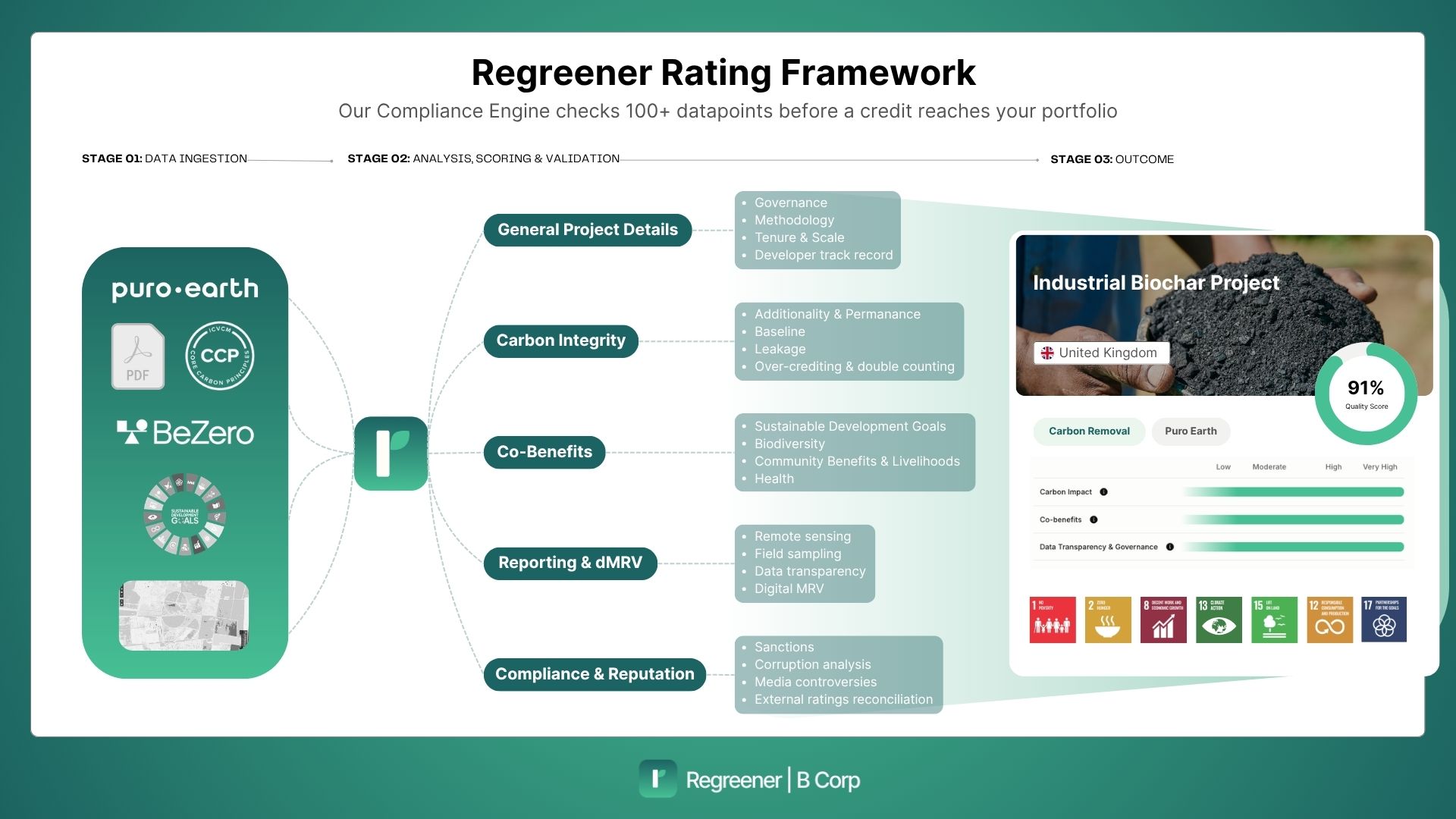

We assess offtake projects against a structured framework spanning five risk domains, scoring each project before any client commits. We use independent ratings from BeZero and Sylvera as anchors, apply benefit-of-the-doubt scoring transparently, and pair the project assessment with a contract review, because a strong project on a weak contract is still a weak deal. For the underlying quality logic, see our carbon credit quality framework. For how this fits the wider procurement decision, see our guide to carbon offtake agreements and our breakdown of offtake versus annual purchasing.

Your next move

Do not treat this as a form to file. Before you sign anything, run all six domains against the specific project in front of you, and write down the answer to one question for each clause you cannot fully verify: what happens to our targets if this goes wrong. If you cannot answer it, you are not ready to commit.

Pull the project's registry record, its independent rating, and the draft contract, and work the checklist top to bottom. Where the project is strong but the contract is thin, fix the clauses before you fix your signature to them. The cost of getting this wrong is not one bad year of credits. It is a decade locked to a counterparty that cannot deliver.

Want to know which credits fit your company's climate strategy?

Book a free consultation today