The price per tonne is the number everyone looks at first. It is almost never where the real value of a carbon credit offtake agreement is decided. The value sits in the clauses underneath: how volume is structured, what happens if the project under-delivers, who carries reversal risk, and which events excuse non-performance. Get those wrong and a "good price" becomes an expensive problem five years in.

This article is the clause-level companion to our full guide to carbon offtake agreements. If you need the basics first, start there. If you already know what an offtake is and want to understand what is actually in the contract, read on.

The key contract terms in a carbon credit offtake agreement

A carbon credit offtake agreement is built around eight contract terms that determine commercial value and risk allocation: volume and delivery schedule, pricing mechanism, quality criteria, make good and replacement provisions, reversal risk and buffer obligations, representations and warranties, force majeure, and termination rights. Each of these clauses is negotiated separately. Each can shift the economics of the deal by more than the headline price.

Volume and delivery schedule

Volume is rarely a single number. A 100,000-tonne offtake is usually a total contract volume delivered as annual tranches over the project's crediting period, with delivery triggered by registry issuance rather than by the project activity itself.

Three volume structures dominate the market:

Fixed volume. The seller commits to deliver a defined number of credits each year. If they don't, a shortfall event is triggered. Strongest position for the buyer, highest risk for the seller.

Unit contingent. The buyer takes whatever the project actually produces, up to a target volume. No shortfall is triggered if the project under-issues. Strongest position for the seller, common in early-stage removal projects where issuance forecasts carry real uncertainty.

Min/max range. A floor and ceiling are agreed. The seller must deliver at least the minimum, the buyer must take up to the maximum. Splits the volume risk between the parties.

Most disputes start here, because the wording of "delivery" is so often loose. Always tie delivery to the date credits land in the buyer's registry account, not the project verification date or the issuance request date.

Pricing mechanism

Three pricing models are standard, with hybrids appearing more frequently as the market matures.

Fixed price. A single per-credit price for the entire contract term. Simple, clean, and exposed in both directions if the market moves significantly.

Fixed escalating. The starting price is fixed with a defined annual uplift, often 2 to 5 percent. Common in five to fifteen year offtakes where both parties expect prices to rise but want certainty about by how much.

Floating or indexed. Price tracks a benchmark, an external index, or a basket of comparable transactions. Used when both parties want exposure to market dynamics rather than a private view on future prices.

Payment timing is a separate negotiation. Pay-on-delivery is standard. Milestone payments tied to project development stages are common in pre-issuance offtakes. Upfront payments shift project finance risk to the buyer and should only be made against meaningful protections elsewhere in the contract. For current price ranges by methodology, see our analysis of carbon credit prices and forecasts.

Quality criteria and credit specifications

Quality is where buyers either protect themselves or, more often, fail to. A well-drafted quality clause locks in:

Registry and methodology. Verra VCS, Gold Standard, Puro.earth, Isometric, Woodland Carbon Code, ACR, or CAR. Specify the exact methodology and version, because methodology revisions can materially affect issuance volumes mid-contract.

Vintage range. The years in which credits must be issued. Without this, sellers can deliver older vintages that may have lower market value or stronger integrity concerns.

Independent rating floors. Increasingly, contracts reference a minimum rating from BeZero Carbon, Sylvera, or Calyx Global. A BeZero AA or Sylvera A floor is now standard in serious removal offtakes and is one of the cleaner ways to write a quality threshold that does not depend on registry rules alone.

Co-benefits and SDG references. Where social, biodiversity, or community claims are part of the buyer's communications strategy, the contract should specify what is required and how it is verified.

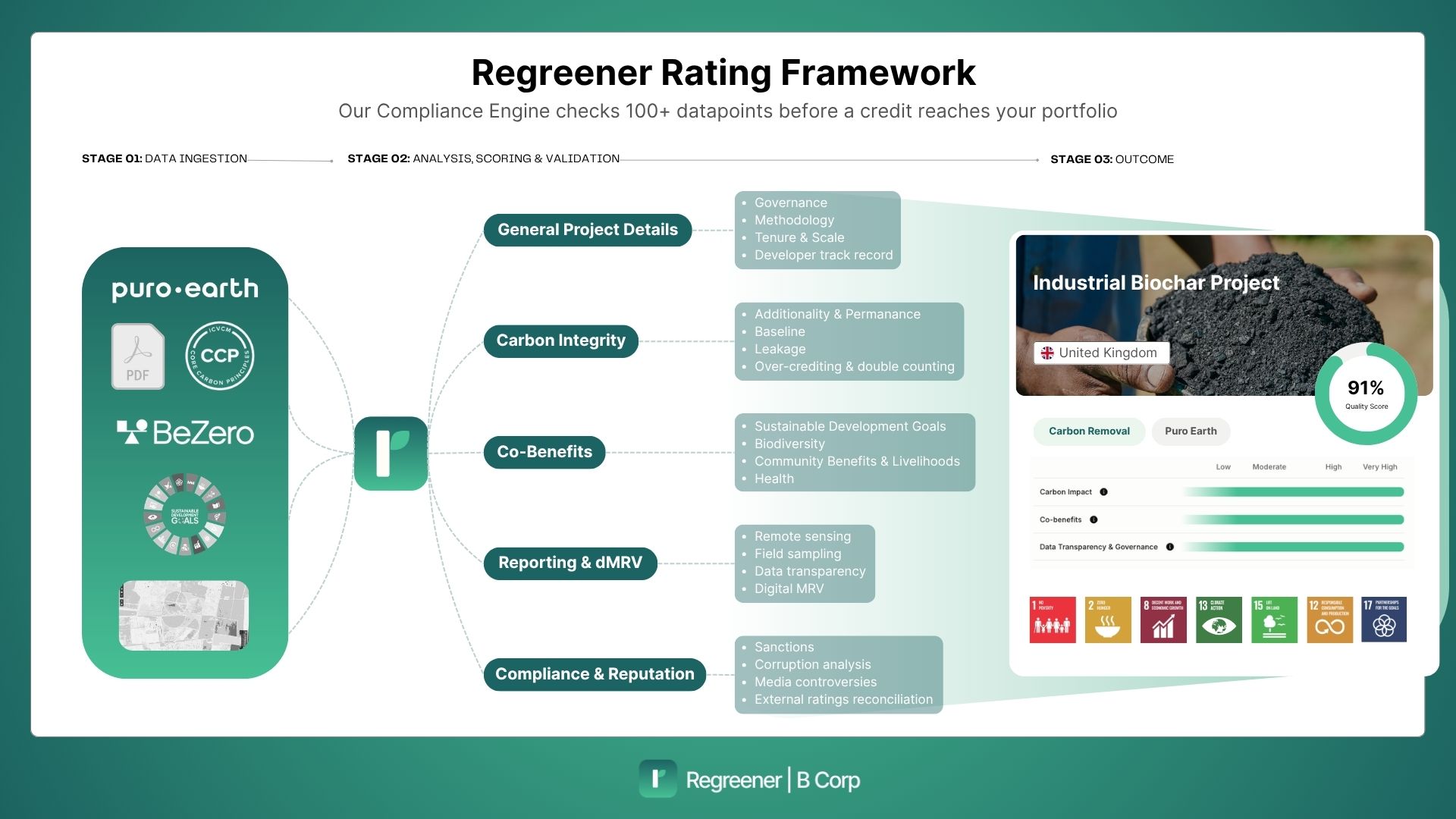

At Regreener we routinely insert independent rating floors into client offtakes and assess every project against more than 100 data points before recommending it. The clause-level work is what makes a quality claim defensible later, when a sustainability report is being audited or a marketing claim is being scrutinised under the EU Green Claims Directive.

Make good and replacement clauses

The make good clause is the single most under-negotiated provision in carbon offtake agreements. It defines what happens if the project under-delivers.

A well-drafted make good clause gives the seller a defined set of cure options rather than triggering immediate default. Typical options include:

Replacement from a backup pool. The seller delivers equivalent credits from another project in their portfolio. The contract should specify quality equivalence: same registry, same vintage range, same rating floor.

Delivery extension. The seller is given additional time to cure the shortfall, often in exchange for an increased delivery volume.

Liquidated damages. A defined dollar-per-credit payment for the shortfall. Sellers want a cap on total damages, buyers want either no cap or one set high enough to preserve performance incentives.

The trade-off is straightforward. Uncapped liquidated damages worry sellers because they can exceed the value of the contract. Capped damages worry buyers because, beyond the cap, the seller has no further financial incentive to deliver. A capped LD paired with a delivery extension and a backup pool obligation is usually the workable middle ground.

Reversal risk and buffer pool obligations

Reversal risk is the carbon-specific risk that has no equivalent in renewable energy contracts. A forest can burn. Soil carbon can be tilled out. A geological storage site can leak. A reforestation project can be felled. Once credits have been issued and retired, the climate impact they represented can disappear.

Two layers of protection are standard. The first is the registry-level buffer pool. Verra, Gold Standard, and the Woodland Carbon Code all withhold a percentage of issued credits in a shared reserve to cover losses across all projects in their portfolios. The percentage varies by methodology and project risk profile.

The second is contractual. Beyond the registry buffer, the offtake should specify what happens if a reversal event affects credits already delivered. Some contracts require the seller to top up the buffer pool. Others require replacement credits to be delivered from the seller's wider portfolio. Some leave the buyer carrying the residual risk, which is rarely the right answer for a serious corporate buyer.

The direction of travel is towards more structured reversal provisions. In October 2025, the UN's Article 6.4 Supervisory Body agreed rules for managing reversal risks in Paris Agreement removal credits, which will shape how reversal clauses are drafted in voluntary contracts as well.

Representations, warranties, and title transfer

The seller's representations form the buyer's protection against legal and regulatory defects in the credits themselves. Standard reps in a carbon offtake include:

Clear and unencumbered title to the credits at the point of delivery

No prior sale, transfer, or pledge of the same credits

No double-counting, double-issuance, or double-claim

Compliance with the relevant registry's rules and the underlying methodology

The project's compliance with applicable host-country law and any Article 6 corresponding adjustment requirements

Title transfer is usually defined as the moment credits are transferred into the buyer's registry account. Before that moment, the credits sit on the seller's risk. After that moment, the buyer carries them. This sounds obvious. It is regularly drafted ambiguously, which creates real problems if a credit is later challenged.

Indemnification scope and survival periods are negotiated alongside the reps. A typical structure caps indemnification at the contract value, with a survival period running several years past the final delivery, since registry challenges and methodology revisions can surface long after a transaction closes.

Force majeure and excused performance

Force majeure provisions in carbon offtakes have to do work that standard commercial FM clauses were not designed for. Beyond the usual catalogue of war, natural disaster, and government action, a well-drafted carbon FM clause should address:

Registry suspension or methodology withdrawal. What happens if Verra suspends a methodology mid-contract and the project can no longer issue credits?

Change in law affecting credit validity. What happens if a new regulation invalidates the type of credit being delivered, as has happened with several REDD+ methodologies?

The interaction with reversal events. Is a wildfire that destroys a reforestation project a force majeure event that excuses delivery, or is it precisely the risk the buffer pool exists to cover? The answer should be in the contract, not in a future dispute.

Force majeure is one of the most-negotiated clauses in long-term offtakes for a reason. The clause distributes the burden of events neither party caused, and the default position in most commercial contracts is heavily seller-friendly. Buyers should push for specificity.

Termination, default, and exit rights

Termination clauses define when and how the parties can walk away. The questions to settle in drafting are:

What constitutes a material default? Repeated delivery shortfalls, a quality failure, an integrity breach, or insolvency are common triggers.

What cure period applies before default becomes terminable?

What are the buyer-side termination rights when the seller fails to deliver, when project quality degrades, or when the seller is acquired by an entity the buyer does not want to do business with?

What are the seller-side termination rights for buyer non-payment?

What happens to credits already delivered versus credits not yet issued? Delivered credits typically remain the buyer's property. Future credits revert to the seller, with any pre-paid amounts refunded on a pro-rata basis.

Termination is where the contract's risk allocation becomes visible. A contract that is generous on volume and pricing but tight on the buyer's exit rights is not the deal it appears to be.

Curious what an offtake could do for your climate strategy?

Carbon offtake agreements are no longer just for hyperscalers and oil majors. UK and EU corporate buyers with multi-year net-zero commitments are using them to lock in tomorrow's high-integrity supply at today's prices, secure access to projects that will be fully subscribed within years, and turn their carbon spend from an annual cost into a strategic asset.

Whether that case applies to your business depends on your emissions trajectory, your reporting obligations, and the methodologies that fit your strategy. We help corporate buyers think it through and structure offtakes that make commercial and climate sense from the start.

Talk to Regreener about building your offtake →

Want to know which credits fit your company's climate strategy?

Book a free consultation today